La oferta de polipropileno commodity de China se concentra en tres grupos estatales — Sinopec, PetroChina y CNOOC — más un puñado de complejos privados de segundo nivel en línea desde 2020. Aproximadamente tres cuartas partes de la capacidad nacional de PP se encuentra en ese conjunto, y China agregará 21,92 millones de toneladas de nueva capacidad entre 2024 y 2028, alrededor del 45% de cada adición global.

La lista corta a continuación clasifica a los proveedores según qué ranura de grado es el canal natural para cada productor — copolímero aleatorio de tubería PP-R, homopolímero de monofilamento, PP para bolsas tejidas, copolímero de inyección — no por ingresos. Los grupos estatales aparecen primero como suministro principal; los privados de segundo nivel siguen como segundas fuentes específicas de ranura; tres grandes globales cierran como puntos de referencia.

Sinopec — Cobertura de Ranura de Grado Más Amplia

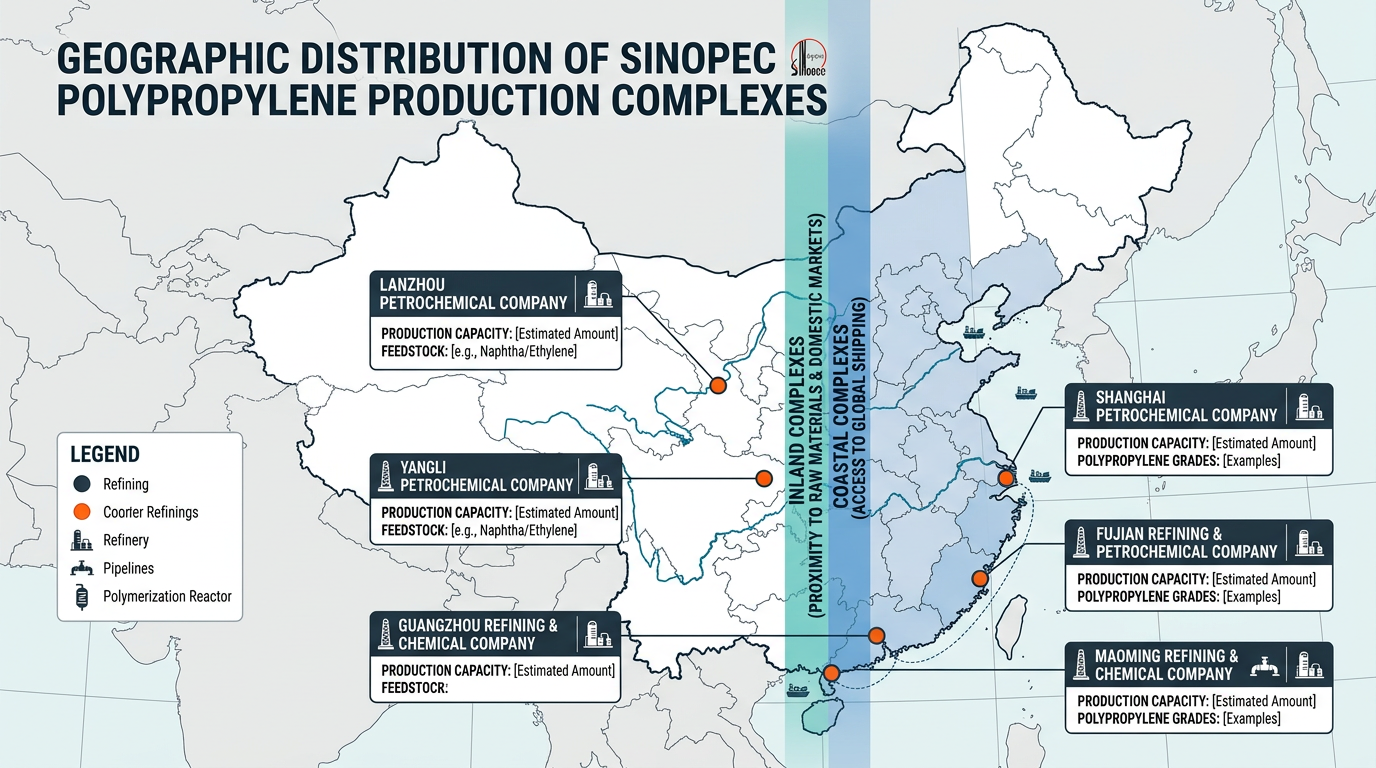

Sinopec opera 17 plantas de PP en toda China con capacidad superior a 7 millones de toneladas por año, distribuidas en los complejos de Maoming, Yanshan (Pekín), Zhenhai (Ningbo), Anqing, Qilu y Yangzi. Casi cada ranura de commodity — homopolímero para bolsas tejidas (S1003), homopolímero de monofilamento (T30S), copolímero aleatorio PP-R, copolímero de impacto para automoción — tiene un equivalente de Sinopec en uno de esos sitios.

Un T30S de Maoming y un T30S de Zhenhai cumplen la misma ficha técnica, pero el flete, el formato del COA y el plazo de entrega de la documentación difieren entre complejos. Los complejos costeros (Zhenhai, Maoming) tienen una prima de precio del 5-10% sobre los sitios del interior por consistencia del servicio.

PetroChina — Dushanzi T4401 Es la Referencia de Tubería PP-R

El complejo Dushanzi de PetroChina en Xinjiang opera una unidad de 550 KTA con licencia de INEOS Unidad Innovene de PP, puesta en marcha en agosto de 2009. El copolímero aleatorio Dushanzi T4401 (0.25-0.30 g/10min MFI) es la referencia del grupo PetroChina para tuberías de agua caliente y fría de PP-R — el caballo de batalla para PP-R en Europa y el Sudeste Asiático compounders europeos y del sudeste asiático que abastecen un canal chino. Los equivalentes de Sinopec de Yanshan o Zhenhai se negocian en bandas paralelas.

PetroChina también ofrece homopolímero de monofilamento T30S desde múltiples sitios. El pedigrí del proceso Innovene es un contexto útil para los compradores que aún tratan al PP estatal chino como de segundo nivel en calidad.

CNOOC — Capacidad de Huizhou para FCL Costero

El complejo de refinación-petroquímica de CNOOC en Huizhou alberga la capacidad principal de PP del grupo y sirve al tráfico de exportación costero del sur de China. Para los compradores de carga completa que envían desde Guangzhou o Shenzhen, CNOOC Huizhou a menudo supera a los sitios de PetroChina en el interior en flete FCL incluso cuando el precio por tonelada de resina es ligeramente más alto.

La lista de grados se superpone con Sinopec y PetroChina en las ranuras de bolsas tejidas e inyección; el diferenciador es la logística. CNOOC se sitúa naturalmente como la segunda fuente del sur de China frente a un primario de Sinopec o PetroChina en el norte.

Zhejiang Petrochemical (Rongsheng) — Spherizone a Escala Privada

El Zhejiang Petrochemical de Rongsheng en la isla Dayushan opera un complejo integrado de 40 millones de tpy; su planta de PP utiliza el proceso Spherizone con licencia de LyondellBasell — tecnología de reactor bimodal que produce grados de amplia distribución de peso molecular que coinciden con la producción del proceso Innovene.

La brecha tecnológica entre los privados de segundo nivel y los grandes estatales se cerró aquí primero. Lo que aún los separa para el trabajo de exportación es la consistencia del formato del COA y la continuidad de los documentos de envío — califique a Zhejiang Petrochemical como una segunda fuente específica de ranura, no como un primario.

Hengli Petrochemical — Grados de Rafia e Inyección de Dalian

Hengli opera una base de refinación de crudo de 20 millones de tpy en Dalian. La línea de productos de PP incluye PPH-T035 (homopolímero para rafia/bolsas tejidas, L5E89) y PPB-M03 (copolímero de inyección de baja fluidez, K8003), punto de fusión 164-170 °C, densidad 0,90-0,91 g/cm³.

Hengli desempeña bien las ranuras de bolsas tejidas e inyección. El complejo está situado tierra adentro desde el puerto de Dalian, por lo que la economía del FCL costero es más ajustada que la de CNOOC Huizhou para el mismo grado.

Shenghong Petrochemical — Recién Llegado de Lianyungang

Jiangsu Eastern Shenghong puso en marcha un complejo de refinación-petroquímica de 16 millones de tpy en Lianyungang en diciembre de 2022. Los grados de PP aún se están estableciendo con los compounders internacionales; los lotes de prueba de calificación son la primera conversación típica.

Para los compradores dispuestos a realizar la calificación, la ubicación costera de Shenghong en Jiangsu supera a los sitios costeros de Sinopec en negocios al contado.

Wanhua Chemical — Alcance de Grado Especializado

La capacidad de PP commodity de Wanhua es menor que la de los tres principales grupos estatales, pero el grupo aporta grados especializados de poliolefinas — copolímeros especializados de alto flujo y reología controlada — que la línea estatal centrada en commodities no cubre adecuadamente. Wanhua está en la mayoría de las listas cortas de los compounders como un suplemento especializado, no como un proveedor principal.

Si la aplicación necesita un grado commodity en volumen, Wanhua no es la primera llamada; si necesita una modificación especializada, Wanhua lo es.

LyondellBasell — Líder Global en Capacidad

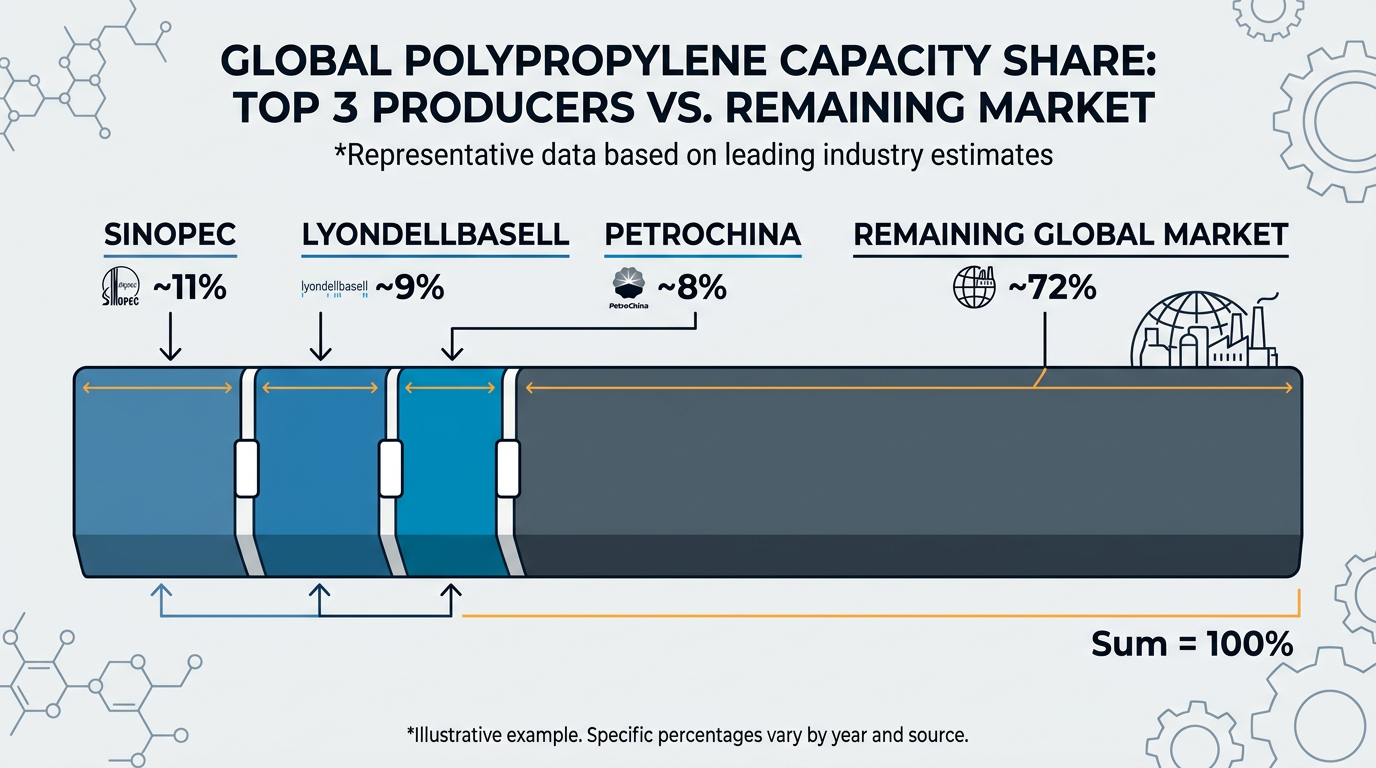

LyondellBasell es el líder del mercado global de PP por capacidad y cartera de productos; junto con Sinopec y SABIC, los tres controlan conjuntamente más del 25% de la capacidad global de PP. Para el abastecimiento a través del canal chino, LyondellBasell aparece con mayor frecuencia como el licenciante del proceso detrás del Spherizone PP de Zhejiang Petrochemical, no como un canal de suministro directo a China.

Cuando un compounder europeo califica una segunda fuente china frente al suministro europeo existente de LyondellBasell, LyondellBasell es la línea base de especificaciones.

ExxonMobil — Referencia del Top-5 y Líder en Circularidad

ExxonMobil se encuentra entre los cinco principales productores de PP de Mordor Intelligence 2025-2026 y lidera el impulso del PP circular desde su unidad de reciclaje avanzado en Baytown. Para los compradores del canal chino, ExxonMobil refleja a LyondellBasell — una línea base de especificaciones global y referencia de circularidad ESG, no un canal de suministro directo a China.

Los compounders europeos bajo presión de balance de masa mantienen el PP certificado ISCC de ExxonMobil en la lista de proveedores calificados incluso cuando el volumen comercial se desplaza a los canales chinos.

SABIC — Volumen de Oriente Medio hacia Asia

SABIC completa la alineación global de los cinco principales. El flujo asiático de SABIC llega a los compounders del sudeste asiático y a China como materia prima importada, compitiendo con el PP estatal chino por los mismos compounders costeros.

Para los compradores internacionales que utilizan China como una región de abastecimiento, SABIC es la verificación cruzada de Oriente Medio: especificaciones estándar, geografía diferente, exposición arancelaria diferente.

Cómo utilizar esta lista corta

Elija un proveedor principal estatal (Sinopec, PetroChina o CNOOC) anclado en el grado que la aplicación demande, y califique una segunda fuente dentro del mismo grupo. Cambiar entre grupos estatales introduce diferencias en el formato del COA y en los documentos de envío que retrasan los envíos FCL.

Una asignación viable asigna 60% al proveedor principal y 40% al de respaldo, con la capacidad de cambiar al 100% en cuatro semanas cuando un complejo entra en parada. La selección del canal es una decisión; la decisión de la familia de grados — homopolímero frente a copolímero aleatorio frente a copolímero de impacto — es la siguiente, una vez que el canal está fijado.